.png)

Dear Patrons,

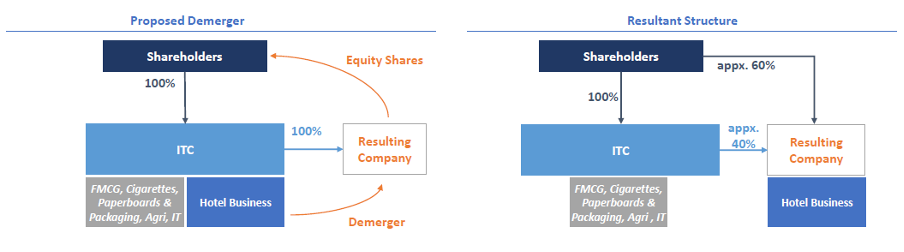

In its exchange filing, ITC Ltd. announced that the board has accorded in-principle approval for the demerger of its hotel’s business. Under the proposed scheme, the company would hold stake of ~40% while the balance would be held by the company’s shareholders proportionate to their shareholding in the company (refer exhibit 1). The demerged entity will be a wholly owned subsidiary, “ITC Hotels Limited” or any other name as may be approved by the relevant authorities.

Exhibit 1: ITC shareholders to get direct stake in a pure play listed Hotel entity

Source: Company, Ambit Asset Management

Strategic Rationale

After two years of pandemic-led disruption, the Indian hospitality industry has witnessed a remarkable recovery, with revenue and profits growing significantly due to increased business travels, weddings, leisure, and return of the MICE (meetings, incentives, conferences, and exhibitions) segments. The company stated that:

- The hotels business is well poised to chart its own growth path as a separate entity with a sharper focus on the hotels and hospitality business whilst continuing to leverage ITC’s institutional strengths, brand equity and goodwill.

- New entity would operate with an optimal capital structure, with the ability to access equity / debt markets for funding growth requirements.

- Unlock Value for ITC shareholders: Independent market driven valuation of focused new entity.

- The company believes that the demerger will help the new subsidiary attract appropriate investors and strategic partners whose investment strategies and risk profiles aligns more with that of the hospitality industry.

About the Hotels segment

Over the last two decades, ITC has scaled to over 120 hotels and 11,600 keys across over 70 locations. Having achieved considerable scale, the business pivoted to an ‘asset-right’ strategy in 2018, which envisages a substantial part of incremental room additions to accrue through management contracts. It has presence across a wide range of price points: 40% of the room inventory is in the Luxury segment, followed by the premium/ upscale segment (30% share) and mid-market (refer exhibit 2).

Exhibit 2: Apart from the brands below, ITC also operates one luxury hotel in Delhi under the Sheraton brand

Source: Company, Ambit Asset Management

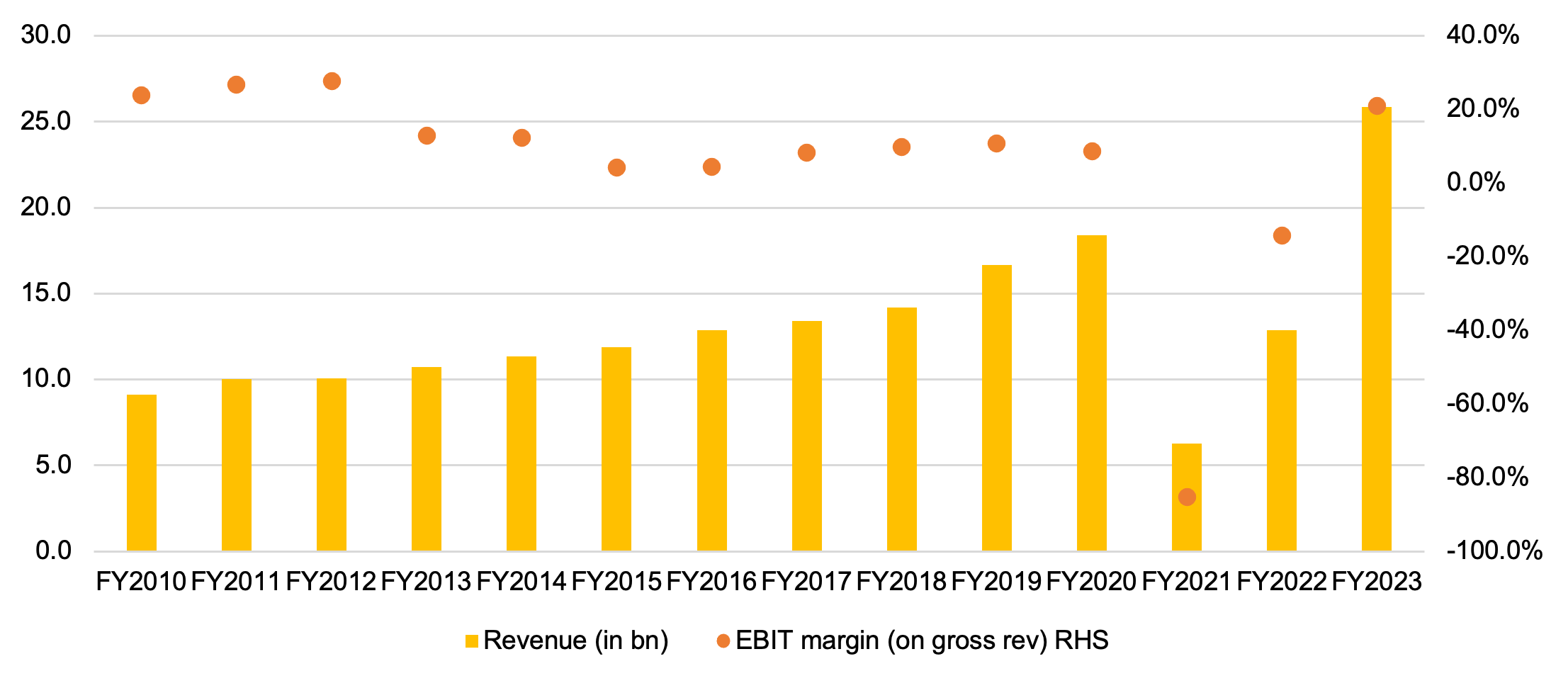

ITC's hotel business has faced pressures in the last decade, due to cyclicality of the business, and the subdued average room rates even as it kept adding new hotel properties. Covid-19 further impacted the business in FY21/FY22. However, the segment witnessed recovery in FY23 on the back of the wedding season, leisure and business travel.

Exhibit 3: ITC hotels business grew by 5% CAGR till 2018; grew by 12% CAGR from FY18-23

Source: Company, Ambit Asset Management

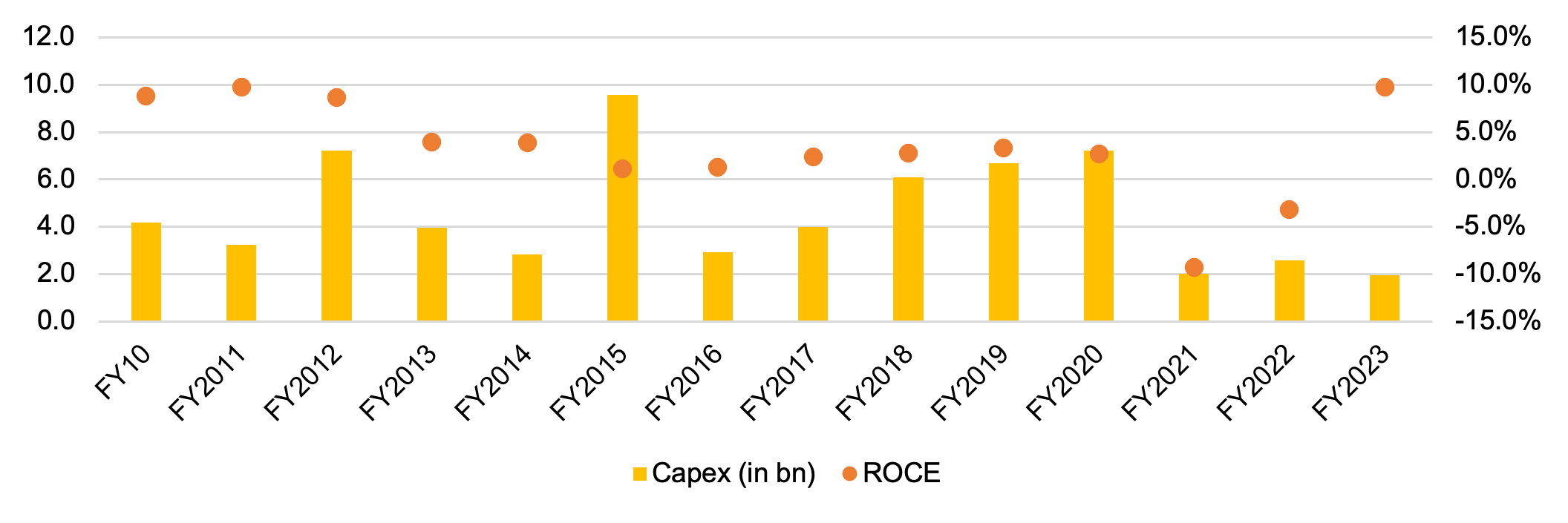

The hotel business contributed less than 5% of ITC revenues and EBIT over the last decade. However, it accounted for over 20% of the company's capex. The high capex on the hotels business and the resultant subpar returns have always been a concern. Hotel business accounted for nearly a quarter of ITC's capex over FY10-20 with <5% RoCEs. The demerger will, thus, help unlock the value of the hotel’s business for the company’s shareholders by providing them with a direct stake in the new entity and an independent market-driven valuation. The hotel business contributed less than 5% of ITC revenues and EBIT over the last decade. However, it accounted for over 20% of the company's capex.

Exhibit 4: High capex intensity and weak return ratios in the hotel business have been a key concern

Source: Company, Ambit Asset Management

Key takeaways from management commentary

- Aim of the current structure (40:60 structures) in the new entity is to provide: a) stability to the new entity, b) access to brand assets and domain expertise, and c) comfort to stakeholders, including partners and employees. The company will continue to leverage cross-segment learnings for employees going ahead, which will be facilitated by their respective boards.

- The scheme of demerger is likely to be tax neutral for all parties — ITC, the new entity, and shareholders.

- ITC will enter into a Royalty arrangement with ITC Hotels. For usage of ITC and its brands, there would be an arrangement regarding royalty, based on industry benchmarks.

- Management sees a ~18-20% points expansion in ROCE and a ~10% points expansion in ROIC, for FY23..

The Going ahead, any further stake dilution will be the decision of the Board and contingent on the situation at that point in time. Also, management is clear that the shareholder will take an independent call, with respect to their holding in the new entity. ITC is not looking to buy-back shares from existing shareholders.

Conclusion

In alignment with the company’s ‘ITC Next’ strategy, the demerger emphasizes on sharper capital allocation, future growth, and unlocking value for shareholders. With focus on better profitability and enhanced competitiveness, the demerger aligns with ITC’s principles of agile operations, consumer centricity and innovation. While value unlocking owing to demerger of the Hotels business is unlikely to be material, we see improvement in ITC’s returns profile, post demerger of hotel operations.

For any queries, please contact:

Umang Shah - Phone: +91 22 6623 3281, Email - aiapms@ambit.co. Registered Address: Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Corporate Address: Ambit Investment Advisors Private Limited - 2103/2104, 21st Floor, One Lodha Place, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.